Any important financial decision starts with understanding the cost structure. Although many companies aim to increase their turnover, few analyze in depth fixed/variable costs structure and how it impacts the margin and financial balance.

In this article, we clearly explain:

-

- what are fixed costs

- what are variable costs

- what is the difference between them

- how do they impact profitability

- how can you optimize your cost structure for company healthy growth

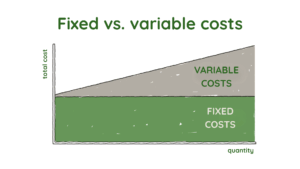

What are fixed costs

Fixed costs are those expenses that generally remain constant on the short term, regardless of the company activity volume. In other words, you incur them even if you sell more or less.

Examples of fixed costs:

-

- rent for headquarters or production space

- administrative salaries

- equipment depreciation

- insurance

- software subscriptions

- various monthly services

- bank commissions

Their essential characteristic is that they do not depend directly on the volume of production or sales. The problem arises when the level of fixed costs is too high in relation to revenue. In this case, the company becomes vulnerable to declines in activity.

What are variable costs

Variable costs are expenses that vary depending on the company activity volume. The more you produce or sell, the more they increase.

Examples of variable costs:

-

- raw materials and supplies

- direct production costs

- sales commissions

- transportation and logistics per unit

- packaging

- performance-related bonuses

Their essential characteristic is that they are directly related to the company activity level. Variable costs directly influence the gross margin and profitability of each product or service.

Difference between fixed costs and variable costs

In short, the difference lies in the way they react to variations in activity volume. Fixed costs generally remain at the same level, regardless of whether you sell more or less. In contrast, variable costs adjust with activity, they increase when you produce or sell more and decrease when the volume decreases.

This difference is essential for:

-

- calculate the break-even point

- pricing

- profitability analysis

- financial planning

- operational risk assessment

A company with very high fixed costs needs a constant volume of sales to remain profitable. A company with a higher share of variable costs has more flexibility in difficult times.

How cost structure affects profit

Profit depends not only on how much you sell, but also on how costs are distributed in relation to income.

Contribution margin is the difference between income and variable costs and reflects the way in which each sale contributes to covering fixed costs and generating profit.

If contribution margin is low due to high variable costs, increasing volume may not generate proportional profit. If fixed costs are too high, any temporary drop in sales can seriously affect profitability.

That is why cost structure analysis must be a central step in the financial planning process.

At ELFWISE, within the financial analyses we perform for companies, cost structure is one of the first elements evaluated, as it directly influences financial stability and growth capacity.

Costs role in break-even point calculation

The break-even point represents the sales level at which incomes exactly cover total costs (fixed + variable), without profit and without loss.

The simplified formula is:

Fixed costs / contribution margin = minimum volume required for break-even

Without a clear limit between fixed and variable costs, the break-even calculation is imprecise, and decisions can become risky.

What are mixed costs

In practice, not all costs are completely fixed or completely variable.

There are also mixed costs, which include a fixed and a variable component. Examples:

-

- utility bills (fixed part + variable consumption)

- salaries with a fixed component and a variable bonus

- outsourced services partially paid per volume

In financial analysis, costs must be broken down into fixed and variable components, in order to correctly understand their impact on the company profit and cash flow.

How do you optimize cost structure

Costs optimization does not necessarily mean aggressive reduction, but alignment with the business model. Align your expenses with your business strategy and your actual income. The objective is to create a sustainable structure that protects your margins and supports growth.

1. Clearly separate fixed and variable costs

Understand which expenses remain constant and which depend on volume. This differentiation indicates you the operational risk level and the minimum sales threshold required for profitability.

2. Analyze profitability by segment

Evaluate margin by product, customer and business line. Direct resources to areas of real profitability and reduce exposure to low-margin segments.

3. Eliminate inefficient indirect costs

Identify expenses that do not generate direct value, such as redundant processes, oversized services, and non-optimized contracts.

4. Increase structure flexibility

Where possible, transform fixed costs into variable costs through outsourcing or flexible contracts. This reduces pressure on the company cash flow and operational risk.

5. Align costs with growth objectives

Any adjustment must be reported to the company’s strategic direction. A properly sized cost structure supports investments and maintains control over operating margins.

An optimized structure provides financial flexibility, resilience in unstable periods and the ability to grow without major imbalances.

Frequently asked questions on fixed and variable costs

What is the difference between fixed and variable costs?

Fixed costs remain constant regardless of the activity volume, while variable costs increase or decrease depending on it.

Why is their differentiation important?

It is important in order to correctly calculate profitability, the break-even point and to build a realistic financial plan.

Can fixed costs become variable?

In certain situations, yes, through contract renegotiation or outsourcing.

How do variable costs affect the company’s selling price?

Variable costs directly influence the contribution margin and the minimum price level required for profitability.

How does cost structure influence business risk?

Cost structure determines the operational risk level. A high share of fixed costs reflects a profit more sensitive to sales variations, while a more flexible structure with variable costs reduces risk during downturns.

How can you identify if your cost structure is optimal?

By analyzing contribution margin, break-even point and profitability by segment (products, customers, business lines). An optimal structure supports both profitability and flexibility in the face of market changes.

Conclusion

The structure of fixed and variable costs directly influences your business stability and profitability. A well-understood cost structure shows you how much you need to sell, how well you can withstand difficult times and how much space you have for investments.

Sustainable growth reflects the balance between income and expenses. If you want a clear cost structure analysis in your company and optimization solutions, the ELFWISE team can support you with a results-oriented financial approach.